Applying for a personal loan has never been easier. Today, you can complete nearly the whole process online—from checking your eligibility, to uploading documents, to getting pre approved. But what does personal loan pre approval online really mean? How does it work, and why should you care? If you’re thinking about borrowing money for a big purchase, to pay off debt, or handle an emergency, understanding online pre approval can make the loan process smoother and less stressful.

This guide explains how online pre approval works, what you need to qualify, and how to avoid common mistakes. By the end, you’ll know how to use pre approval as a tool to get the best deal, save time, and increase your chances of loan approval.

What Is Personal Loan Pre Approval Online?

Personal loan pre approval is when a lender checks your basic details and tells you if you are likely to get a loan. This is not a full approval—it’s more like a green light to go ahead and apply. When you do this online, you can get an answer quickly, often in minutes.

Pre approval is not a promise to lend you money, but it’s a strong sign you meet the lender’s basic criteria. The lender checks things like your credit score, income, and other debts. If you pass, you may get a pre approval letter or offer that shows the loan amount, possible interest rate, and repayment terms.

Why Lenders Offer Pre Approval

Lenders use pre approval to find good customers and reduce their risk. It also helps them process full applications faster, since most of your information has already been checked.

How Does Online Pre Approval Work?

When you apply for personal loan pre approval online, the process is simple and fast. Here’s what usually happens:

- You fill out a form on the lender’s website. This asks for your name, address, income, job details, and sometimes your Social Security number.

- The lender does a soft credit check. This doesn’t hurt your credit score. It’s a quick look at your history to see if you pay bills on time and how much debt you have.

- You get a pre approval decision. This may appear instantly or within a few hours.

- If you’re pre approved, you’ll see possible loan terms—how much you can borrow, the interest rate, and the repayment period.

It’s important to know that pre approval is not a guarantee. You’ll need to submit more documents and the lender will do a full credit check before final approval.

Benefits Of Getting Pre Approved Online

There are clear reasons why more people are using online pre approval for personal loans:

- Speed: You can get an answer in minutes, not days.

- Convenience: Apply from home, work, or anywhere with internet.

- Comparison: Pre approval lets you see different offers without hurting your credit.

- Confidence: You know your chances before applying, which saves time and effort.

- Privacy: No need for face-to-face meetings or phone calls.

What Do Lenders Check For Pre Approval?

Lenders want to know if you’re a safe bet. Here’s what they usually look at:

- Credit score: Most lenders have a minimum score (often 600–650).

- Income: You need to show you can repay the loan. Some lenders want proof of steady income for at least 6–12 months.

- Debt-to-income ratio (DTI): This is your monthly debt payments divided by your income. Many lenders prefer a DTI below 40%.

- Employment status: Full-time work is best, but some accept self-employed or part-time workers.

- Residency: You usually need to be a US citizen or permanent resident.

Here’s a quick comparison of basic pre approval requirements from three major US lenders:

| Lender | Min. Credit Score | Min. Income | Max DTI |

|---|---|---|---|

| SoFi | 680 | $45,000/year | 40% |

| Marcus by Goldman Sachs | 660 | $30,000/year | 45% |

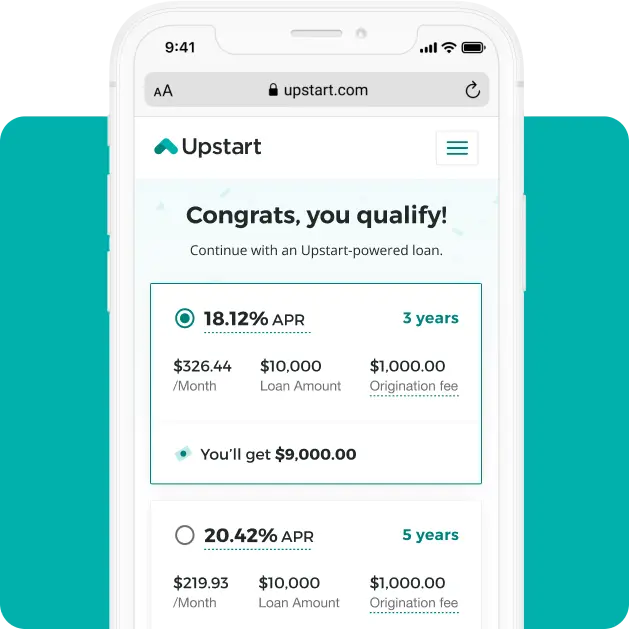

| Upstart | 600 | $12,000/year | 50% |

Steps To Get Pre Approved For A Personal Loan Online

To get the best results, follow these clear steps:

- Check your credit report. Fix any errors before applying.

- Calculate your budget. Know how much you want to borrow and what you can afford to pay monthly.

- Research lenders. Look for those that offer pre approval with a soft credit check.

- Gather documents. You may need pay stubs, tax returns, and bank statements for later steps.

- Fill out the online form. Be honest—lenders will verify your details.

- Compare offers. Look at the interest rate, fees, and repayment terms.

- Choose the best offer and apply. Now the lender will do a full review and ask for more documents.

- Get your funds. If approved, money is usually sent to your bank account within 1–5 days.

Common Mistakes To Avoid

Even with a simple online process, people make errors that can lead to delays or denials:

- Applying with incorrect information. Don’t guess your income or job title—lenders will check.

- Ignoring your credit score. If your score is low, work to improve it before applying.

- Not comparing offers. The first offer may not be the best. Always shop around.

- Borrowing more than you need. Larger loans mean higher monthly payments and more interest.

- Missing hidden fees. Watch for origination fees, prepayment penalties, or insurance add-ons.

A useful tip: Some lenders advertise “no fees”, but check the fine print. For example, some may not charge an origination fee, but have higher interest rates instead.

How Pre Approval Affects Your Credit Score

The good news is that most online pre approval checks use a soft inquiry. This does not lower your credit score. But if you move ahead and apply for the loan, the lender will do a hard inquiry, which can drop your score by a few points. Multiple hard inquiries in a short time can hurt your score more.

If you’re shopping around, do all your full applications within two weeks. Credit scoring models often count these as one inquiry if they’re close together.

Comparing Pre Approval Offers

Once you get pre approved by several lenders, it’s time to compare offers. Look beyond just the interest rate. Here’s a sample comparison table of three pre approval offers:

| Lender | Loan Amount | Interest Rate (APR) | Monthly Payment | Origination Fee |

|---|---|---|---|---|

| Lender A | $10,000 | 9.5% | $210 | $0 |

| Lender B | $10,000 | 8.9% | $207 | $350 |

| Lender C | $10,000 | 10.2% | $215 | $0 |

Notice that the lowest interest rate isn’t always the cheapest overall if there are high fees. Be sure to look at the APR (annual percentage rate), which includes fees and interest.

Pre Approval Vs. Pre Qualification

Many people mix up pre approval with pre qualification. They sound similar, but they’re not the same.

- Pre qualification is a quick, informal estimate. The lender may not check your credit or details closely.

- Pre approval is more detailed. The lender checks your credit and verifies some of your information. It carries more weight.

If you want to show sellers or partners you’re serious, a pre approval letter is much stronger than a pre qualification.

What Happens After Pre Approval?

After you’re pre approved, you’re invited to complete a full application. Here’s what usually happens next:

- Document upload: You provide pay stubs, tax returns, or ID online.

- Full credit check: The lender does a hard inquiry.

- Final decision: You get a final approval or denial, usually within 1–3 business days.

- Sign loan agreement: This is often done electronically.

- Receive funds: Money is sent directly to your bank account, sometimes the same day.

If any information doesn’t match what you gave during pre approval, your loan may be denied.

Security And Privacy With Online Pre Approval

People often worry about entering personal details online. Reputable lenders use encryption to protect your data. Look for “https” in the website address and check for privacy policies. Never share your bank login info or Social Security number by email or text.

For more on keeping your data safe, the Federal Trade Commission offers practical tips.

Who Should Use Online Pre Approval?

Online pre approval is a good fit if you:

- Want to compare multiple loan offers quickly.

- Need money fast and can’t visit a bank.

- Have a good or fair credit score (600+).

- Prefer digital paperwork and e-signatures.

If you have poor credit or a complicated financial situation, you might have better luck talking to a lender in person.

When To Avoid Pre Approval

There are times when pre approval is not the best move:

- If you know you won’t qualify (low income, poor credit).

- If you’re not ready to borrow yet—pre approval offers are often valid for only 30–60 days.

- If you’re worried about your data privacy and don’t trust online forms.

Practical Insights Most Beginners Miss

- Your pre approval offer may change. If your income, debts, or credit score change before you finish your full application, the lender may offer a lower amount or higher rate—or deny the loan.

- Some lenders do a hard inquiry for pre approval. While most use soft inquiries, a few do not. Always check before applying. Too many hard inquiries can lower your score.

- Pre approval does not lock in your rate. Interest rates may rise or fall before you complete the full application. Move quickly if you find a good deal.

- Check for loan amount limits. Some lenders have higher minimums or lower maximums for online loans than in-branch loans.

- You can use pre approval to negotiate. If you have multiple offers, you can sometimes ask your preferred lender to match or beat another lender’s rate.

:max_bytes(150000):strip_icc()/how-to-get-a-personal-loan-online-7569494-final-1014065af49f4ef4830d0714ca4ab7b0.png)

Frequently Asked Questions

What Is The Difference Between Pre Approval And Final Approval?

Pre approval is a first check to see if you qualify for a loan. You still need to provide documents and pass a full review before getting final approval and your money.

Does Online Pre Approval Affect My Credit Score?

Most online pre approval checks use a soft inquiry that does not hurt your credit score. Only a full loan application causes a hard inquiry, which may lower your score by a few points.

How Long Does Personal Loan Pre Approval Last?

Most pre approval offers are valid for 30 to 60 days. If you don’t finish your application in that time, you may need to apply again.

Can I Get Pre Approved For More Than One Personal Loan At A Time?

Yes, you can get pre approved by several lenders. This helps you compare offers and find the best deal. Just avoid submitting too many full applications, as multiple hard inquiries can lower your credit score.

What Documents Do I Need For Personal Loan Pre Approval Online?

For pre approval, you usually only need basic details—name, address, income, and sometimes your Social Security number. For final approval, you’ll need to provide proof of income, employment verification, and ID documents.

Applying for a personal loan pre approval online can be a smart way to find out where you stand, compare your options, and speed up the loan process. By understanding how it works and avoiding common mistakes, you give yourself the best chance for success—without risking your credit score or wasting time on offers you can’t get. As with any financial decision, read the fine print, ask questions, and choose the loan that fits your needs best.

Read More:

- Best Term Life Insurance Companies: Top Picks for 2026

- Insurance Explained: Smart Tips to Protect Your Future Today

- Homeowners Insurance Quote: How to Save Big on Your Policy

- Compare Auto Insurance Rates: Find the Best Deals in Minutes

- Car Insurance Quotes Online: Compare Rates and Save Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Debt Consolidation Loan Rates: How to Find the Best Deal

- Best Mortgage Refinance Rates: Unlock the Lowest Rates Today