When debt starts to pile up, it can feel overwhelming. Many people face high-interest credit cards, medical bills, or personal loans. Managing several payments is stressful, and it’s easy to lose track. One solution that’s getting more attention is the debt consolidation loan. This type of loan lets you combine your debts into a single payment, often at a lower interest rate. But before you jump in, it’s important to understand how debt consolidation loan rates work, what affects them, and how to get the best deal. In this article, you’ll get clear, practical advice to help you make smart choices.

What Is A Debt Consolidation Loan?

A debt consolidation loan is a financial tool that helps you combine multiple debts into one new loan. This new loan usually has a single interest rate and a fixed monthly payment. The main goal is to make your debt easier to manage and, if possible, to reduce the total interest you pay.

For example, if you have three credit cards with balances and a personal loan, you might use a debt consolidation loan to pay off all four. Then, you only have one payment each month. This can reduce stress and help you avoid late fees.

Key benefits:

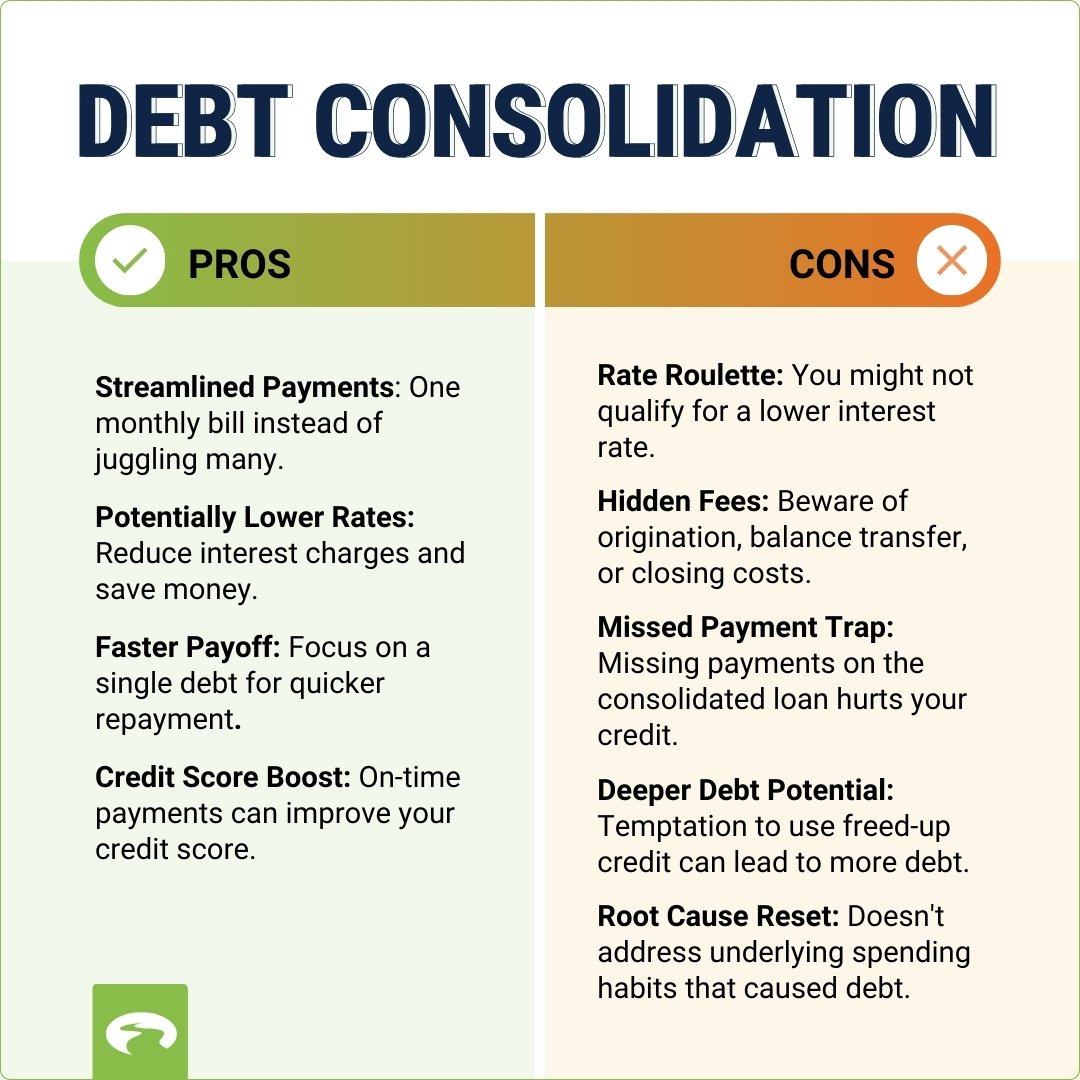

- Simplifies your finances (one payment instead of many)

- May lower your interest rate

- Can improve your credit score over time if you pay on time

But not all debt consolidation loans are equal. The interest rate you get matters a lot. Let’s look at what affects these rates.

Factors That Affect Debt Consolidation Loan Rates

Debt consolidation loan rates are not fixed for everyone. They depend on many things. Understanding these factors can help you get a better rate.

Credit Score

Your credit score is one of the biggest factors. Lenders look at your score to decide how risky you are. If your score is high (above 700), you’ll likely get a lower rate. If it’s low (below 600), your rate will be higher.

Income And Debt-to-income Ratio

Lenders check your income and compare it to your debts. This is called the debt-to-income ratio. If you earn more and owe less, you’re safer for the lender, so you may get a better rate.

Loan Amount And Term

The size of your loan and how long you’ll take to repay it (the term) also matter. Larger loans or longer terms may have higher rates. Shorter-term loans often have lower rates, but payments are higher.

Type Of Loan

Some debt consolidation loans are secured (backed by assets like your house), while others are unsecured (no collateral). Secured loans usually have lower rates but more risk. If you miss payments, you could lose your asset.

Lender Choice

Different lenders offer different rates. Banks, credit unions, and online lenders all compete. It’s smart to shop around.

Here’s a simple table showing how these factors can change your rate:

| Factor | Low Rate Example | High Rate Example |

|---|---|---|

| Credit Score | 750+ | Below 600 |

| Debt-to-Income | 20% | 50% |

| Loan Term | 2 years | 7 years |

| Loan Type | Secured | Unsecured |

| Lender | Credit Union | Online lender |

Typical Debt Consolidation Loan Rates (2024)

Debt consolidation loan rates change often. In 2024, most rates range from 6% to 36% APR (Annual Percentage Rate). Your actual rate depends on your situation.

- Excellent credit (720+): 6%–12% APR

- Good credit (680–719): 12%–20% APR

- Fair credit (620–679): 20%–28% APR

- Poor credit (below 620): 28%–36% APR

Some lenders may charge extra fees, so always check the full cost. Here’s a comparison table of rates by credit score:

| Credit Score | APR Range | Typical Fees |

|---|---|---|

| Excellent (720+) | 6%–12% | 1%–3% |

| Good (680–719) | 12%–20% | 3%–5% |

| Fair (620–679) | 20%–28% | 5%–7% |

| Poor (below 620) | 28%–36% | 7%–10% |

Real Example

Imagine you have $10,000 in credit card debt at 20% APR. You get a debt consolidation loan at 10% APR for 3 years. Your monthly payment drops, and you save money on interest. Over three years, you could save about $1,800 in interest.

How To Qualify For The Best Debt Consolidation Loan Rates

Getting a low rate is possible if you prepare well. Here are practical steps:

- Check your credit report. Fix errors and pay down debts to boost your score.

- Compare lenders. Don’t settle for the first offer. Use online tools to see different rates.

- Consider secured loans if you have assets and feel comfortable. But understand the risks.

- Choose a shorter term if you can afford higher payments. This often lowers your rate.

- Avoid adding new debts before applying. Lenders want to see stable finances.

Many beginners miss two key points:

- Some lenders let you prequalify without hurting your credit score. Use this to check your rate before applying.

- If your loan has fees, calculate the total cost, not just the interest rate. Sometimes a low rate comes with high fees.

Comparing Debt Consolidation Loan Rates To Other Options

Debt consolidation loans aren’t the only way to manage debt. You should know how they compare to other popular options.

Credit Card Balance Transfers

Some credit cards offer 0% APR for a limited time if you transfer a balance. But after this period, rates jump—sometimes above 20%. You must pay off the debt before the promo ends, or you’ll pay high interest.

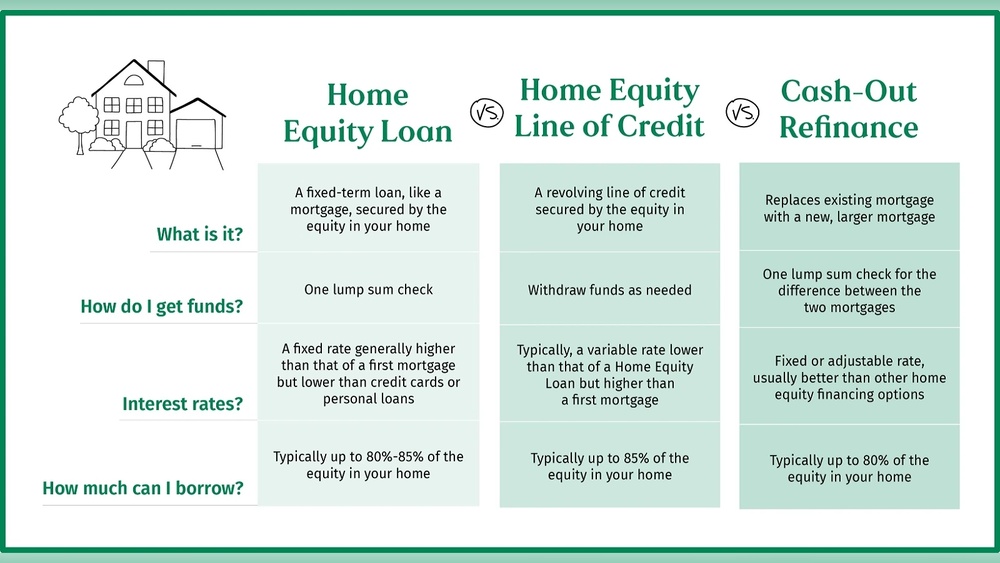

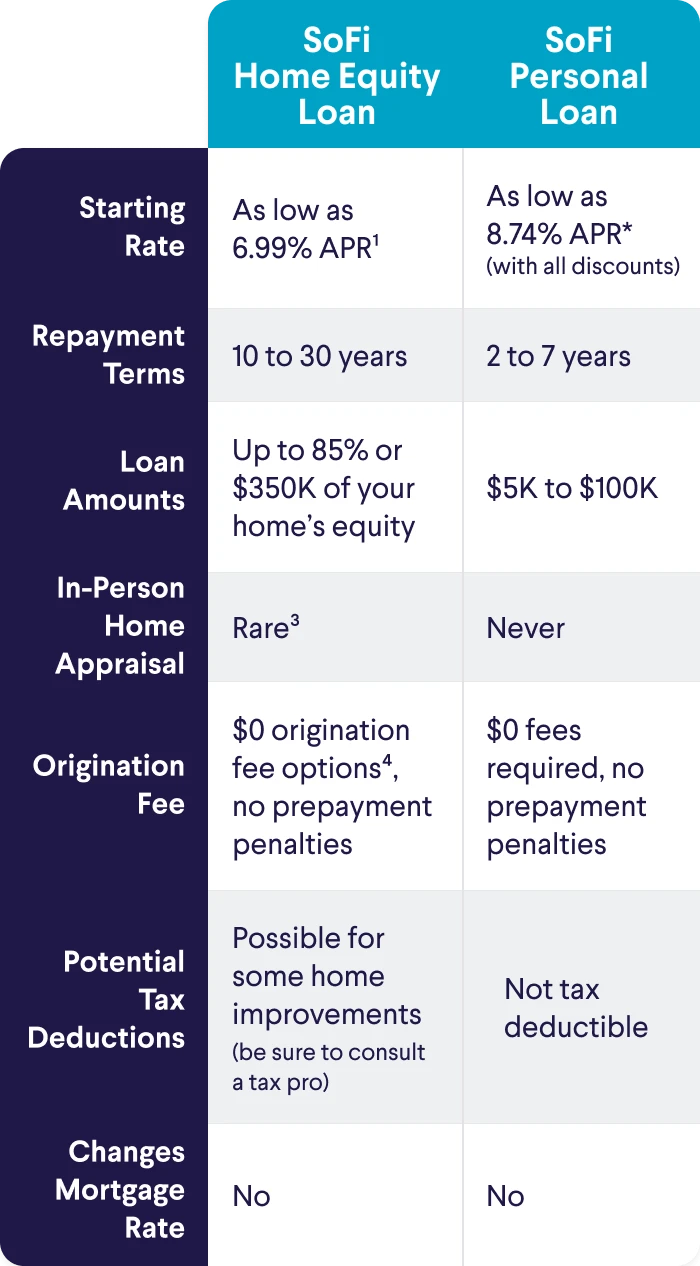

Home Equity Loans

If you own a home, you can use a home equity loan to consolidate debts. Rates are often lower (5%–9%), but your home is at risk if you can’t pay.

Personal Loans

Personal loans are similar to debt consolidation loans. Rates are based on your credit. Some personal loans are marketed as debt consolidation options.

Here’s a comparison table:

| Option | APR Range | Risk | Typical Fees |

|---|---|---|---|

| Debt Consolidation Loan | 6%–36% | Low to medium | 1%–10% |

| Credit Card Balance Transfer | 0%–25% | Medium | 3%–5% |

| Home Equity Loan | 5%–9% | High (home as collateral) | 2%–5% |

| Personal Loan | 6%–36% | Medium | 1%–10% |

Common Mistakes When Choosing Debt Consolidation Loans

People often make mistakes that cost them money or cause stress. Avoid these:

- Not checking your credit report for errors before applying.

- Ignoring fees—some loans have origination fees, late fees, or prepayment penalties.

- Choosing a longer loan term just for lower monthly payments. You may pay more interest over time.

- Not comparing lenders. Rates can vary a lot.

- Missing the fine print. Some loans have tricky terms.

A non-obvious insight: If you consolidate and then keep using your old credit cards, you can end up with even more debt. Close or freeze those accounts if you’re tempted.

When Debt Consolidation Loan Rates Make Sense

Debt consolidation loans are not always the right answer. They work best when:

- Your new rate is lower than your current rates.

- You can handle the monthly payment.

- You’re serious about paying off debt and not adding more.

If your credit is poor, or you don’t qualify for a lower rate, other options may be better. For some, working with a credit counselor can help. They may offer advice or negotiate with lenders.

How To Apply For A Debt Consolidation Loan

Ready to apply? Here’s a step-by-step guide:

- Check your credit score online for free.

- Gather your debt information—balances, interest rates, and monthly payments.

- Shop around. Use online comparison sites or talk to banks and credit unions.

- Prequalify where possible. This lets you see rates without a hard credit check.

- Compare offers. Look at the APR, fees, and terms.

- Read the agreement before signing. Make sure you understand everything.

- Pay off your debts with the loan funds.

- Make payments on time every month.

If you need more guidance, you can visit Consumer Financial Protection Bureau for trusted resources.

Frequently Asked Questions

What Is The Average Debt Consolidation Loan Rate In The Us?

The average rate is around 12%–20% APR for borrowers with good credit. Rates can be lower if you have excellent credit or higher if your credit is poor.

Does Applying For A Debt Consolidation Loan Hurt My Credit Score?

If you apply, the lender will do a hard credit check, which can lower your score by a few points. But if you get the loan and pay off old debts, your score may improve over time.

Can I Get A Debt Consolidation Loan With Bad Credit?

Yes, but your rate will likely be high (28%–36% APR). Some lenders specialize in bad credit loans, but it’s important to compare offers and check for hidden fees.

How Long Does It Take To Get Approved?

Most lenders give an answer within 1–3 business days. Some online lenders are faster. Funding can take a few days after approval.

Is It Better To Choose A Secured Or Unsecured Debt Consolidation Loan?

Secured loans have lower rates but more risk, since you must use an asset as collateral (like your house or car). Unsecured loans are safer for you but have higher rates. Choose based on your comfort and risk level.

Debt consolidation loan rates can make a big difference in your financial life. By understanding how rates work, comparing options, and avoiding common mistakes, you can find the best solution for your needs. Take your time, ask questions, and make a plan that fits your goals.

The right loan can help you get control of your debt—and your future.

Read More:

- Best Term Life Insurance Companies: Top Picks for 2026

- Insurance Explained: Smart Tips to Protect Your Future Today

- Homeowners Insurance Quote: How to Save Big on Your Policy

- Compare Auto Insurance Rates: Find the Best Deals in Minutes

- Car Insurance Quotes Online: Compare Rates and Save Today

- Personal Loan Pre Approval Online: Fast Track Your Approval Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Best Mortgage Refinance Rates: Unlock the Lowest Rates Today