Getting a homeowners insurance quote can feel confusing, especially if it’s your first time. You want to protect your home and belongings, but many people aren’t sure how quotes work, what affects the price, or how to compare different options.

This guide will help you understand everything you need to know, using simple language and practical tips. By the end, you’ll be able to get a quote confidently, know what details matter, and make smart choices for your home.

What Is A Homeowners Insurance Quote?

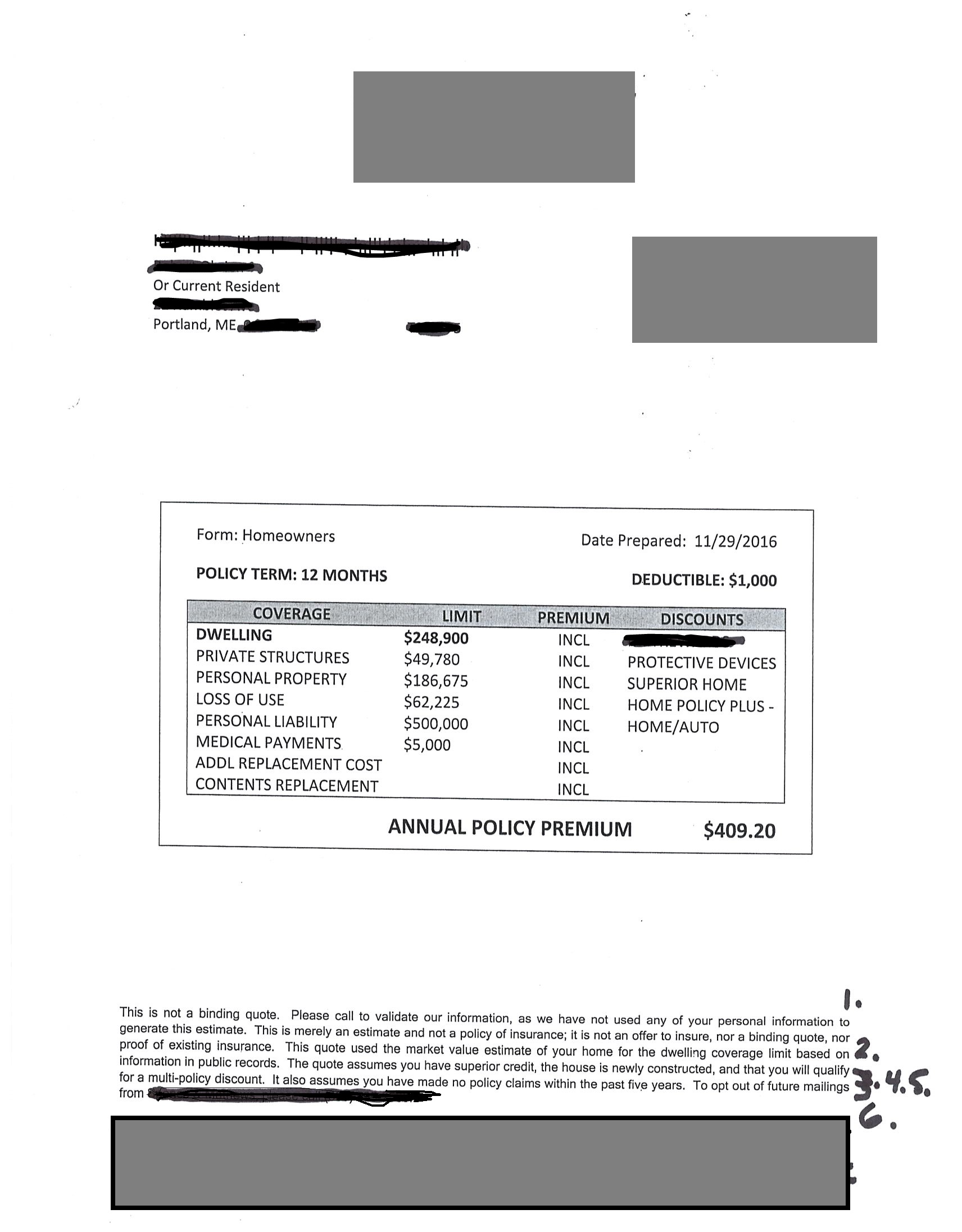

A homeowners insurance quote is an estimate of how much you’ll pay for insurance to protect your house, personal belongings, and liability. Insurance companies use your details—like your address, home value, and safety features—to calculate this price. The quote is not a final price; it can change after the company checks more details or runs a risk assessment.

For example, if you enter your information online, you might see a quote of $1,200 per year. When the company reviews your claim history or inspects your home, the final price could go up or down. Quotes help you compare different insurers before buying a policy.

Why Do You Need A Quote?

Getting a quote before buying insurance is important because:

- Compare prices: Each company uses its own method to calculate prices. You might find big differences.

- Understand coverage: Quotes show what’s included, like fire, theft, or water damage.

- Budget planning: Knowing the cost helps you plan your finances.

- Spot gaps: You can see if important coverage, like flood protection, is missing.

Many homeowners make the mistake of choosing the first quote they get. Comparing at least three quotes can save you hundreds of dollars per year and help you find better coverage.

Key Factors That Affect Your Quote

Insurance companies look at several details to decide your price. Here are the most important:

Location

Your home’s location affects the price the most. Houses in areas with high crime rates or severe weather (like hurricanes or floods) usually cost more to insure. For example, a home in Miami, FL, may cost more than one in Denver, CO.

Home Value And Features

The value of your home, its size, and construction type matter. Brick homes often cost less to insure than wooden ones because they resist fire better. If your house is worth $300,000 and has a new roof, your quote could be lower than a similar home with an old roof.

Coverage Amounts

The more coverage you want, the higher the price. If you want $500,000 coverage instead of $200,000, expect to pay more. Insurers also ask about deductibles—the amount you pay out of pocket before insurance pays. Higher deductibles mean lower premiums.

Security Measures

Homes with security systems, smoke detectors, or deadbolt locks often get discounts. Some companies offer up to 10% off for homes with strong security.

Personal Details

Your credit score, claims history, and even pets can change your quote. People with good credit scores usually pay less. If you filed claims in the past five years, your price will likely go up.

Data Example

Here’s a comparison of how location affects annual homeowners insurance premiums:

| City | Average Annual Premium |

|---|---|

| Houston, TX | $2,100 |

| Phoenix, AZ | $1,000 |

| Boston, MA | $1,400 |

| Miami, FL | $2,800 |

As you can see, location can double or triple your premium.

How To Get A Homeowners Insurance Quote

Getting a quote is easy, but there are a few steps to follow:

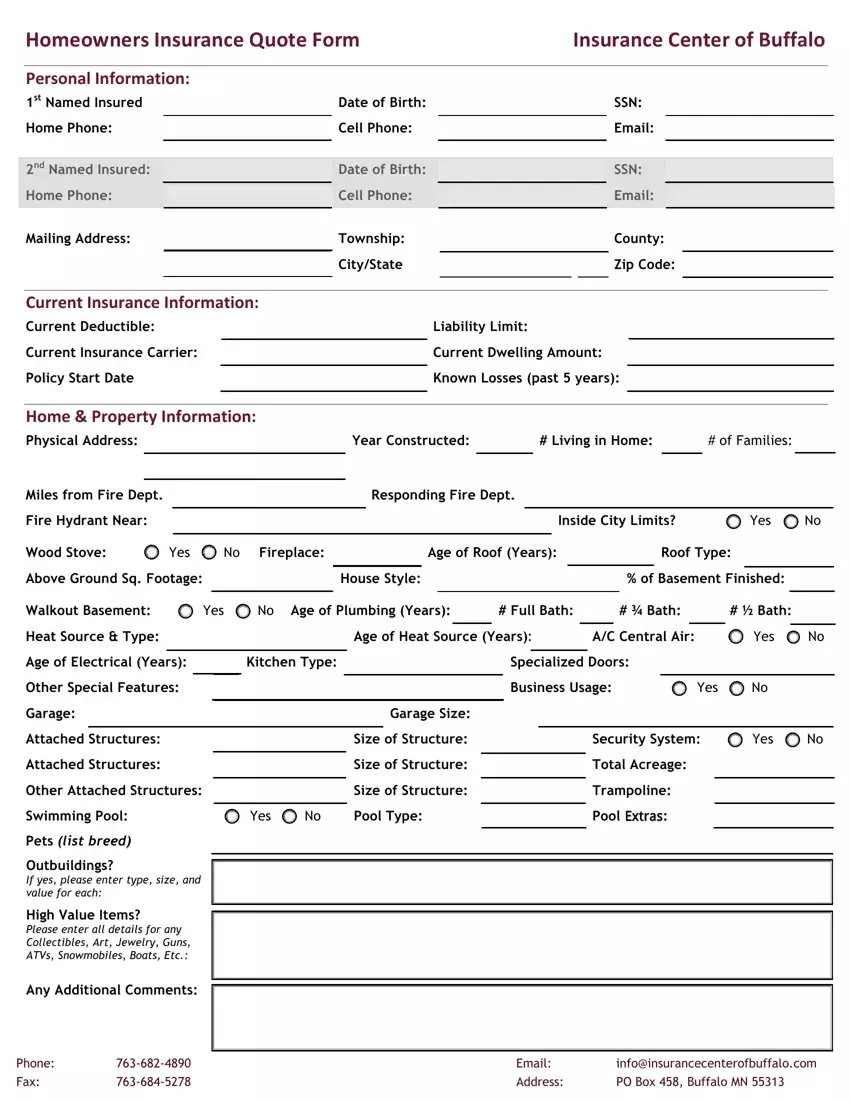

1. Gather Your Home Information

You’ll need:

- Your home’s address

- Year built

- Square footage

- Type of construction (brick, wood, etc.)

- Roof age and material

- Security features (alarms, locks, cameras)

- Value of your personal belongings

Having accurate data helps you get a reliable quote.

2. Decide What Coverage You Need

Standard policies cover the structure, personal items, and liability. You may want extra coverage for:

- Floods

- Earthquakes

- Jewelry or valuables

Think about risks in your area and what you own.

3. Request Quotes

You can get quotes:

- Online (most companies offer forms)

- By phone

- Through an insurance agent

Many people choose online quotes for speed. Make sure to use the same details for each company, so you can compare fairly.

4. Compare Quotes

Look at:

- Price

- Coverage types

- Deductibles

- Discounts

- Customer reviews

Don’t focus only on price. A cheap policy may have gaps that cost you later. Check what’s included and excluded.

Here’s a sample comparison of three quotes for a $250,000 home:

| Company | Annual Premium | Deductible | Water Damage Coverage | Discounts |

|---|---|---|---|---|

| ABC Insurance | $1,050 | $1,000 | Included | 10% for security |

| XYZ Insurance | $1,150 | $500 | Excluded | 5% for new roof |

| HomeSafe | $950 | $1,500 | Included | 15% for bundled auto |

Notice how coverage and discounts change the value, not just the price.

Common Mistakes When Getting Quotes

Even careful homeowners can make mistakes. Here are some to watch for:

- Underestimating home value: If you use a low value, you may get less coverage than you need.

- Ignoring deductibles: A low premium with a high deductible can hurt you during claims.

- Missing discounts: Many forget to mention security systems or bundled auto insurance.

- Not reading exclusions: Policies often exclude floods, earthquakes, or mold. Always check!

- Skipping reviews: Some companies have poor service or slow claims—read customer reviews.

A less obvious mistake is forgetting to update your quote after home changes. If you add a new roof or security system, your premium may drop. Update your quote every year.

What Coverage Options Can You Choose?

Homeowners insurance offers several types of coverage. It’s important to know what each covers.

Dwelling Coverage

Protects the structure of your home from risks like fire, wind, or vandalism.

Personal Property Coverage

Pays for stolen or damaged items inside your home, like furniture, electronics, or clothes.

Liability Coverage

Covers legal costs if someone is hurt on your property and sues you.

Additional Living Expenses

Pays for hotel and food if your home is damaged and you need to live elsewhere.

Special Coverage

You can add coverage for:

- Floods

- Earthquakes

- Jewelry

- Business equipment

Some policies let you raise limits on valuables, which is smart if you have expensive items.

How Insurers Calculate Your Quote

Insurance companies use software and data to estimate your risk. They check your:

- Home value

- Location risk (weather, crime)

- Construction type

- Claim history

- Credit score

- Coverage amounts

- Deductibles

They combine these to create a premium. Here’s a simple breakdown:

| Factor | Impact on Premium |

|---|---|

| Location | High |

| Home Value | Medium |

| Security Features | Low to Medium |

| Claims History | Medium |

| Credit Score | Medium |

A non-obvious insight: Some insurers use satellite and drone images to check roof age and condition, which affects your quote. Keeping your roof in good shape can lower your premium, even if you don’t mention it.

How To Save Money On Your Quote

You can lower your insurance costs with these strategies:

- Raise your deductible: If you can afford a higher out-of-pocket cost during claims, your premium drops.

- Bundle policies: Combine home and auto insurance for discounts up to 20%.

- Upgrade security: Adding alarms, cameras, and deadbolt locks often earns discounts.

- Shop yearly: Prices change, and new discounts appear. Compare every year.

- Improve credit: A better credit score can lower your premium.

Many people miss the chance to save by not bundling or updating their credit score information.

Real-life Example

Sarah owns a home in Dallas, TX, built in 2005. She has a security system and a new roof. She got three quotes:

- $1,500 per year with a $1,000 deductible (no bundling)

- $1,300 per year with a $1,500 deductible (bundled with auto)

- $1,700 per year with a $500 deductible (no security discount)

Sarah chose the second option—higher deductible, but bundled discount. She saved $200 per year and got better coverage.

What Happens After You Get A Quote?

Once you get a quote and choose a company, you apply for coverage. The insurer may:

- Inspect your home

- Check your claim history

- Confirm your details

If everything checks out, you get your policy and start coverage. If they find extra risks (like old wiring), your price may change. Always review your policy before signing.

When Should You Update Your Quote?

Update your quote when:

- You renovate or add rooms

- You install new security systems

- Your home value changes

- You buy expensive items (jewelry, art)

- Your credit score improves

Keeping your insurance up to date helps you stay protected and save money.

Frequently Asked Questions

What Is Included In A Standard Homeowners Insurance Quote?

A standard quote usually includes dwelling coverage, personal property coverage, liability coverage, and additional living expenses. Some quotes may also show optional extras like flood or earthquake coverage. Always check what is included and what is excluded.

How Can I Lower My Homeowners Insurance Quote?

You can lower your quote by raising your deductible, bundling policies (like home and auto), adding security features, and improving your credit score. Shopping around yearly and updating your information can also help.

Why Are Quotes Different From Each Company?

Each insurer uses its own formula for risk and pricing. They weigh factors like location, claims history, and credit score differently. Some companies offer more discounts or cover risks others do not.

Is The Quote The Final Price I Pay?

No, the quote is an estimate. The company may adjust the price after checking your home or claim history. Always read your final policy details before paying.

What Information Do I Need To Get A Quote?

You’ll need your address, home details (year built, size, construction), security features, coverage needs, and sometimes your credit score. Having accurate information gives you a better quote.

Protecting your home is one of the smartest moves you can make. Getting a homeowners insurance quote is the first step toward peace of mind. By understanding the factors, comparing options, and keeping your policy updated, you can save money and stay safe. If you want more details about how insurance works, you can visit National Association of Insurance Commissioners for trusted advice. Remember, the right quote can make all the difference—so take your time, ask questions, and choose wisely.

Read More:

- Best Term Life Insurance Companies: Top Picks for 2026

- Insurance Explained: Smart Tips to Protect Your Future Today

- Compare Auto Insurance Rates: Find the Best Deals in Minutes

- Car Insurance Quotes Online: Compare Rates and Save Today

- Personal Loan Pre Approval Online: Fast Track Your Approval Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Debt Consolidation Loan Rates: How to Find the Best Deal

- Best Mortgage Refinance Rates: Unlock the Lowest Rates Today