Car accidents can be stressful, but handling your insurance claim settlement doesn’t have to be confusing. When you know what to expect, you can move forward with confidence. This guide shows you how to manage the process, explains key factors that influence settlement offers, and highlights mistakes many drivers make. Whether you had a minor fender bender or a major crash, understanding your rights and responsibilities will help you get fair compensation.

Understanding Car Accident Insurance Claims

After a car accident, most drivers file a claim with their auto insurance provider or the other party’s insurer. The claim process starts when you report the accident, describe what happened, and share supporting documents like photos and police reports.

Many Americans don’t realize that the average car insurance claim payout is around $4,000-$5,000 for property damage and over $20,000 for bodily injury (according to the Insurance Information Institute). However, your actual settlement depends on many factors, including the type of coverage you have and who was at fault.

Types Of Coverage

Not all insurance policies are equal. Here’s a quick comparison:

| Coverage Type | What It Pays For | Who Gets Paid |

|---|---|---|

| Liability | Damage and injury to others | Other party |

| Collision | Your car’s repair or replacement | You |

| Comprehensive | Non-collision events (theft, fire) | You |

Most claims after accidents involve liability and collision coverage. If you’re not at fault, you usually file with the other driver’s insurer.

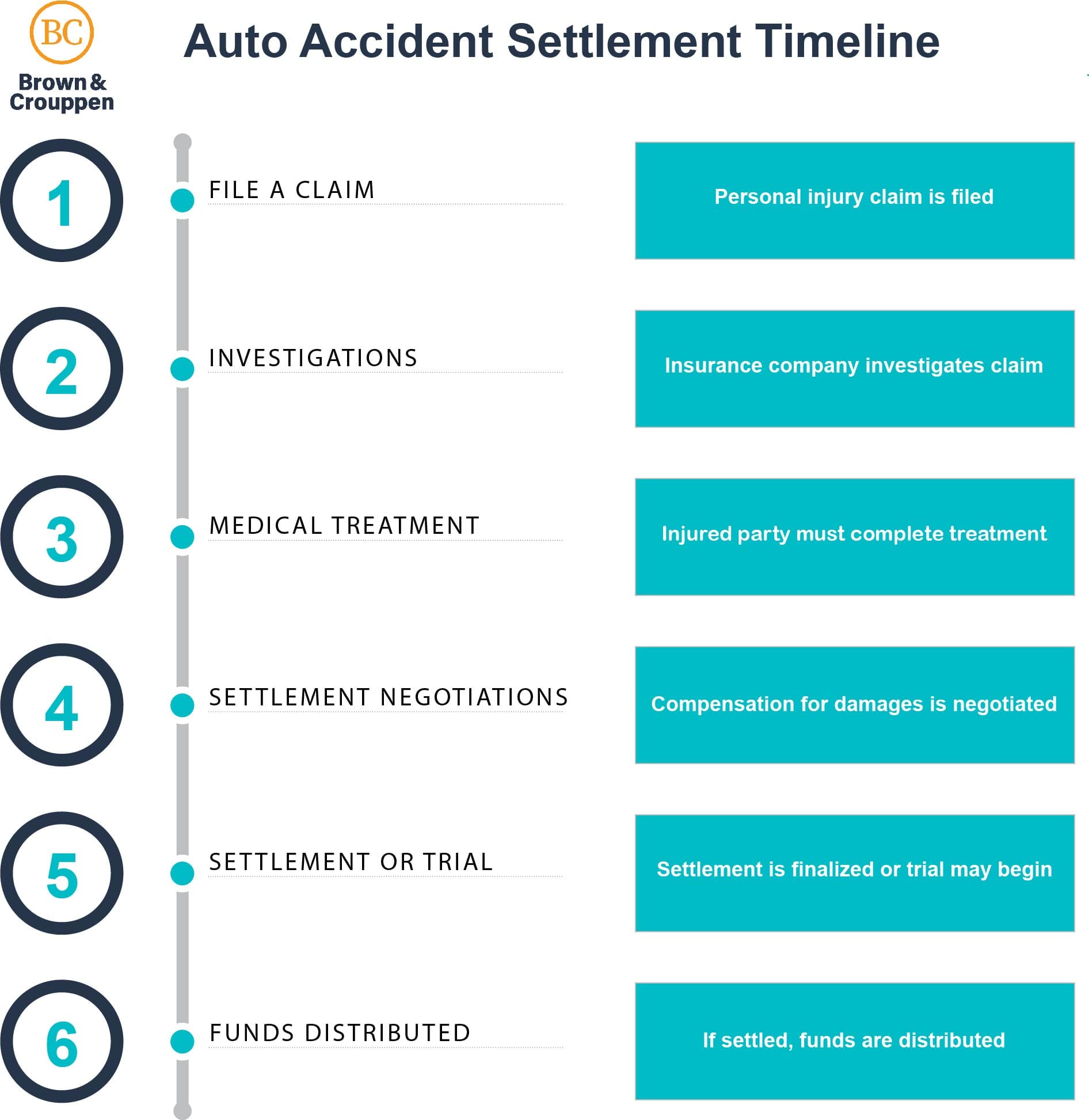

Steps To Settle A Car Accident Claim

Settling your claim doesn’t have to be overwhelming. Here are the main steps:

- Report the accident promptly to your insurer.

- Document everything: Take photos of the scene, damage, and injuries.

- Get a police report if possible.

- Submit required documents to your insurance company.

- Meet with the claims adjuster: They inspect your car and review your case.

- Receive a settlement offer: The adjuster estimates the repair cost or value.

- Negotiate if needed: If the offer seems too low, you can dispute it.

- Accept the offer and sign release forms.

- Receive payment: Funds are sent to you or the repair shop.

Many drivers rush through these steps, but careful documentation and negotiation can make a big difference.

Common Mistakes In The Claim Process

Some mistakes can cost you thousands of dollars. Watch out for these:

- Delaying the claim: Waiting too long can lead to denial.

- Missing evidence: Not taking photos or keeping receipts weakens your claim.

- Admitting fault: Don’t discuss blame at the scene or with insurers until facts are clear.

- Accepting the first offer: Many adjusters start low; challenge their numbers if needed.

How Insurance Companies Calculate Settlements

Insurers use formulas and guidelines to decide how much to pay. Here’s what they consider:

| Factor | Impact on Settlement |

|---|---|

| Car’s market value | Sets maximum payout for repairs or replacement |

| Repair estimates | Directly affects compensation |

| Policy limits | Caps the total payment |

| Fault determination | May reduce payout if you share blame |

| Medical bills | Only paid if coverage includes injury |

For example, if your car is worth $10,000 but repair costs $12,000, your insurer will likely declare it a total loss and pay the actual cash value ($10,000), minus your deductible.

Negotiating For A Better Settlement

Don’t assume the first offer is the best you can get. Here’s how to negotiate:

- Research your car’s value using sites like Kelley Blue Book.

- Get independent repair estimates from trusted shops.

- Present evidence: Share receipts, medical reports, and photos.

- Write a formal letter explaining why the offer is too low.

- Stay calm and professional during discussions.

Most adjusters expect negotiation, and clear evidence can help you get a higher payout. If talks stall, you can ask for a supervisor or consider legal advice.

Special Cases: Injury Claims And Legal Involvement

If you or someone else was injured, the process can become more complex. Injury claims may involve:

- Medical records and bills

- Lost wages

- Pain and suffering

Insurance companies often use a “multiplier method” to estimate pain and suffering—multiplying medical costs by a number between 1. 5 and 5. Serious injuries get higher multipliers.

Sometimes, legal help is necessary. If liability is unclear or the insurer refuses to pay, a lawyer can guide you. In many states, you have 2-3 years to file a lawsuit after an accident.

Tips For Faster And Fair Settlements

- Respond quickly to all insurer requests.

- Keep organized records of calls, emails, and documents.

- Don’t exaggerate damage; honesty builds trust.

- Check your policy for exclusions and limits.

- Ask questions—insurers must explain their decisions.

One insight many drivers miss: Insurers may have preferred repair shops, but you have the right to choose your own. Also, if you’re unhappy with the settlement, you can appeal within the company or through your state’s insurance regulator.

For more guidance, visit the Insurance Information Institute.

Frequently Asked Questions

What Should I Do Right After A Car Accident?

First, make sure everyone is safe. Call the police if needed, take photos of the scene, and exchange information with the other driver. Report the accident to your insurer as soon as possible.

How Long Does It Take To Settle An Insurance Claim?

Most claims are settled within 30-60 days, but complex cases may take longer. Quick responses and complete documents can speed up the process.

Can I Dispute A Low Settlement Offer?

Yes. Gather evidence like repair estimates and medical bills, then write a formal letter to your insurer explaining why their offer is too low. You can escalate the dispute if needed.

What If The Other Driver Doesn’t Have Insurance?

If you have uninsured motorist coverage, your insurer will handle the claim. Otherwise, you may need to sue the other driver or seek help from state compensation funds.

Will My Insurance Rates Go Up After A Claim?

Your rates may increase, especially if you were at fault. Each insurer has its own rules, but a single claim can raise premiums by 20-40% on average.

Handling a car accident insurance claim settlement can be easier if you stay organized and informed. By following the right steps, avoiding common mistakes, and knowing your rights, you can secure a fair payout and get back on the road with confidence.

Read More:

- Best Term Life Insurance Companies: Top Picks for 2026

- Insurance Explained: Smart Tips to Protect Your Future Today

- Homeowners Insurance Quote: How to Save Big on Your Policy

- Compare Auto Insurance Rates: Find the Best Deals in Minutes

- Car Insurance Quotes Online: Compare Rates and Save Today

- Personal Loan Pre Approval Online: Fast Track Your Approval Today

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Debt Consolidation Loan Rates: How to Find the Best Deal